By Kathy Patterson, D.C Auditor

There’s a clear and present danger in the worsening relationship between the District’s elected officials and the District’s independent Chief Financial Officer. Councilmembers are wrapping up their work on the FY 2027 Financial Plan and Budget and CFO Glen Lee is stepping up his warnings of a cash flow crisis 18 months from now.

The danger comes in bad decisions. Contributing is the lack of a shared recognition of what’s real and what’s not in the District’s financial standing. The CFO is damaging his office’s credibility by sounding alarms without adequate explanation. Consider this a fact check.

The CFO’s pronouncements seem to equate cash flow with fund balance, but these are two distinct things.

Yes, Councilmembers are spending down the fund balance. Yes, they’ve done that in the past and continue to do so this year by essentially moving money not spent this year into subsequent fiscal years within the financial plan. They have the authority to do this. If the CFO considers that a bad practice he should explain why. Educating elected officials is a major part of his job.

A declining but still healthy fund balance does little to explain the cash crisis that the CFO claims is imminent. Yet there are significant weaknesses in the numbers that the CFO has NOT been talking about.

General Fund balances

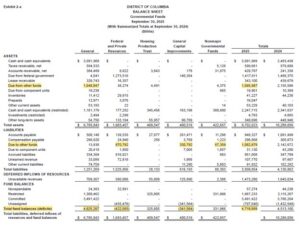

Look at the balance sheet from the FY 2025 Annual Comprehensive Financial Report, below. Notice that the fund balance of the General Fund is $4.8 billion. Then look to the combined fund balance of all governmental funds (namely, the General Fund, Federal & Private Fund, Housing Production Trust Fund, Capital Fund, and every other “nonmajor” fund). The combined fund balance is, surprisingly, less than the fund balance of the General Fund alone. This is the case because the General Fund has loaned almost $1.1 billion to the other funds (see the due to/due from lines)—and, in particular, the Federal and Capital Funds.

Federal Fund balances

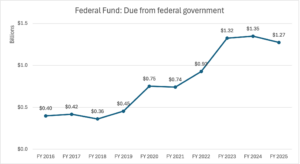

Most worrying is the Federal Fund. The District has a long history of failing to collect federal grants due to poor program administration. The Federal Fund owes the General Fund over $670 million, and the Federal Fund’s biggest asset (by far) is nearly $1.3 billion “Due from federal government.” The feds do tend to pay their bills, so one question is whether the District is actually doing the work, including paperwork, to collect the federal funds that it reports are “due.”

Alternatively, in the current environment it’s possible the Office of Management and Budget initiated a change that results in less cash flowing to the District. It’s important to know which is real: local program failures or less actually owed. Will the District need to consider a disastrous write-down of the amount due from the feds? Could it be “normal” for the feds to owe at this level — 21% of all of the Federal Fund’s revenue in FY 2025?

The uptick in funds owed is clear in recent ACFRs:

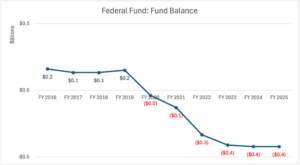

Equally clear is the declining fund balance of the Federal Fund:

The ACFR data shows that the Federal Fund balance has declined as the amount expected from the federal government has increased. But the ACFR data are not presented at a level of detail that would suggest a root cause, that is, one or more specific federal grant programs that are driving these trends.

Then there’s the Capital Fund

As to the Capital Fund, addressing that deficit would require borrowing more money by issuing long-term bonds. But then debt service would rise, another budget pressure. Budgeting more for debt service would affect the multiyear financial plan: the out-years of the plan already put pressure on the District’s 12% cap of debt service as a percentage of the budget. Staying within that cap is said to be very important to the bond-rating agencies.

When the Capital Fund has a deficit (because capital expenditures have been greater than bond proceeds plus operating budget contributions), the fund needs to borrow money from somewhere. Long-term debt is costly to issue and there are disadvantages of borrowing too early. This is why we have the commercial paper program (for which the budget proposes $17.6 million in FY 2027 to pay interest). Commercial paper is designed permit borrowing on a short-term basis only when needed for capital expenditures, and then long-term debt is issued later in tranches that are large enough to pay off the commercial paper and pay for future spending. It is hard to see how the Capital Fund would owe the General Fund $330 million if the commercial paper program were working as intended.

Where’s the cash?

The CFO sees a declining amount of cash in District accounts. If all of these factors are why he is sounding the alarm about cash stability two fiscal years from now, he owes the electeds and the public a much fuller explanation than he’s given. And if he isn’t alarmed by these numbers: why not? If all of this is normal, the CFO should explain where all the cash has gone. And if it’s not normal then the District has done a lousy job at cash management, a core responsibility of the OCFO.

Before there is a final FY 2027 Financial Plan and Budget let’s hope that CFO Lee, Chairman Mendelson and members of the Council do what they need to do to start working from the same set of financial facts.